If you are navigating the Ontario real estate market, you are probably keeping a close eye on interest rates. Whether you are buying your first property, renewing, or expanding an investment portfolio, the interest rate you secure directly impacts your bottom line.

While most Canadians know that the Bank of Canada (BoC) influences our borrowing costs, there is a common misconception that the BoC controls all mortgage rates. In reality, variable and fixed mortgage rates are driven by entirely different financial engines.

If you want to understand where fixed mortgage rates are heading, you need to look away from the Bank of Canada and instead watch the bond market.

Here is a look behind the curtain at exactly how the bond market affects your mortgage, and how you can use this knowledge to make smarter real estate decisions.

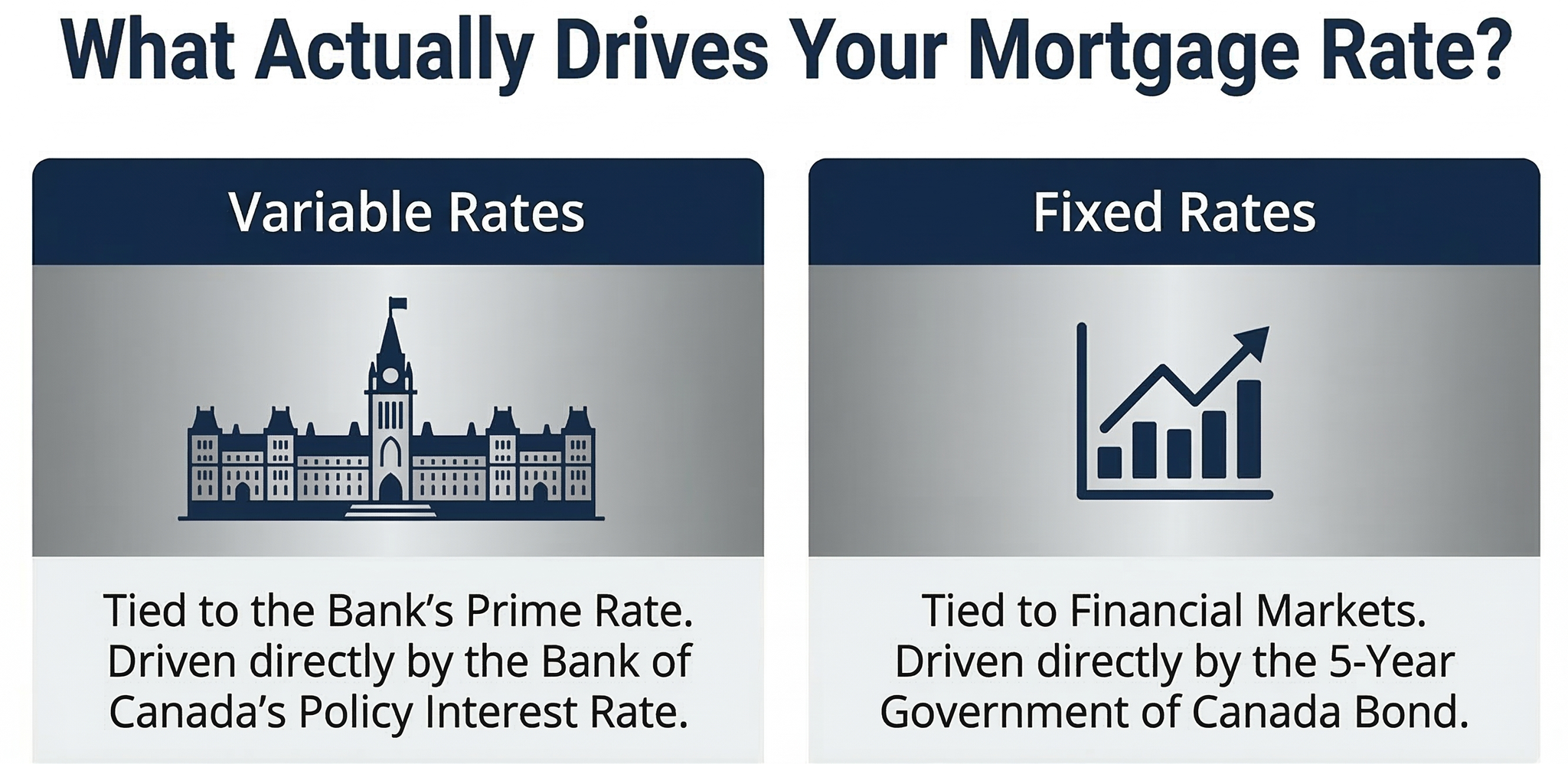

Variable vs. Fixed: A Tale of Two Influencers

To understand the bond market’s role, we first need to separate fixed and variable rates:

- Variable Rates: These are tied directly to your bank’s prime lending rate, which moves in lockstep with the Bank of Canada's policy interest rate.

- Fixed Rates: These are dictated by the financial markets—specifically, Government of Canada bond yields.

What is a Bond Yield?

A bond is essentially a loan from an investor to the government. When the government needs to raise money, it issues bonds. A "bond yield" represents the real rate of return an investor earns for holding that government bond over a set period, such as five years.

Because bonds are traded on public markets, their prices and yields fluctuate daily based on supply, demand, and investor expectations about future inflation and the economy.

How Bond Yields Set Your Fixed Mortgage Rate

Here is exactly how a government bond yield turns into the fixed mortgage rate you are offered at the bank:

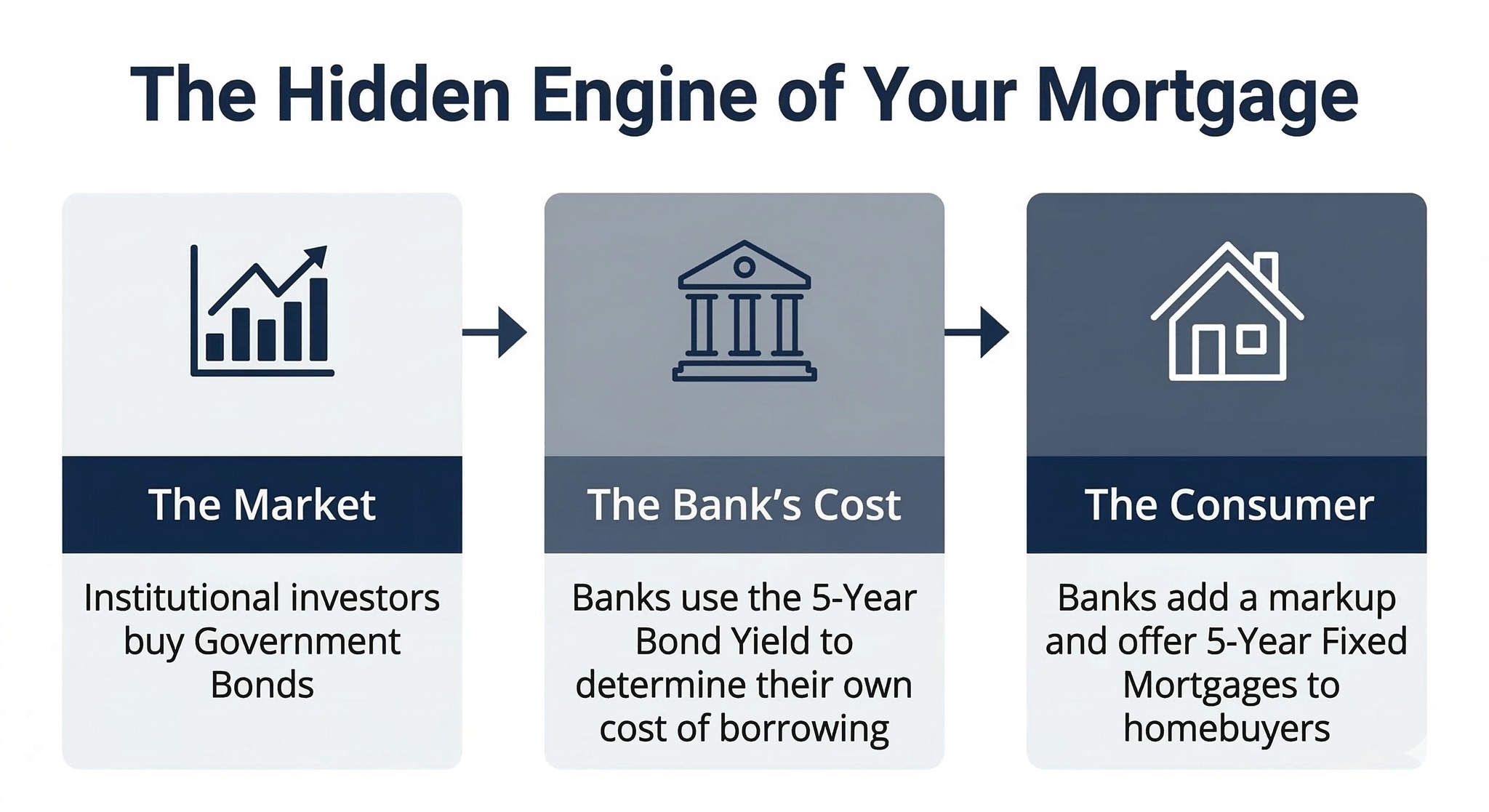

- It Determines the Bank's Cost of Funds When you take out a fixed-rate mortgage, your lender needs to fund that loan. They typically do this by raising capital in the bond markets. If 5-year bond yields rise, it costs the bank more to borrow money for that five-year period. To protect their profit margins, banks will quickly pass those higher funding costs onto you by raising their 5-year fixed mortgage rates. Conversely, if bond yields drop, banks' borrowing costs decrease, allowing them to offer you lower fixed rates.

- The Competition for Capital Banks buy government bonds as a low-maintenance, reliable source of fixed-interest income. Because fixed-rate mortgages compete with these bonds to attract capital, banks use the less-costly bond yields as a baseline to determine how high to set their mortgage rates.

- The "Spread" Of course, lending money to a homebuyer in Ontario carries more risk and higher operational costs than lending money to the Canadian government. Because of this, banks will always set their fixed mortgage rates higher than the current bond yield. In a normal market, this markup—known as the "spread"—is typically between 1% and 2% (100 to 200 basis points) above the government bond yield.

Why Everyone Watches the 5-Year Bond

You will often hear financial analysts specifically discussing the 5-year Government of Canada bond yield. This is simply because the 5-year fixed-rate mortgage is the most popular mortgage term in Canada. Lenders closely monitor the 5-year bond yield because it perfectly aligns with the term length of the product their clients want the most.

What is Happening Right Now?

Bond markets act as a barometer for global economic anxiety. Recently, global geopolitical tensions—specifically the military conflict in Iran—have choked off oil supplies and pushed global oil prices up. Because higher oil prices threaten to drive up inflation, bond traders have demanded higher yields.

As a result, the Canada 5-year bond yield recently spiked to the 3.0% range. True to form, banks responded to these higher funding costs by raising 5-year fixed mortgage rates by about 0.25%.

How to Use This Information

You don't need to be a Wall Street trader to use this to your advantage. If you are within 120 to 150 days of a mortgage renewal or are actively shopping for an Ontario property, keep a casual eye on the 5-year bond yield.

- If bond yields are trending upward steadily over several days, fixed mortgage rates are highly likely to follow soon. This is your signal to act quickly and lock in a rate hold.

- If bond yields are trending down, lenders may soon drop their fixed rates, potentially giving you an opportunity to secure a better deal.

Discuss Your Next Real Estate Move

The multifamily market is shifting rapidly, and having the right data is only half the battle—executing the right strategy is what drives returns. Whether you are looking to expand your portfolio, underwrite a new opportunity, or list an existing asset, I am here to help you navigate the market with confidence.

The multifamily market is shifting rapidly, and having the right data is only half the battle—executing the right strategy is what drives returns. Whether you are looking to expand your portfolio, underwrite a new opportunity, or list an existing asset, I am here to help you navigate the market with confidence.Check out this article next