As we settle into 2026, the landscape for multi-residential investors in Ontario is undergoing a distinct shift. After years of hyper-compressed vacancy rates and double-digit rent growth, the market is catching its breath. For landlords, 2026 will not be about capitalizing on scarcity, but rather about strategic management, tenant retention, and understanding regional nuances.

Drawing on the latest data from CMHC, Stats Canada, MLS surveys and market reports from early 2026, here is what is happening on the ground in Ontario and what you should be watching this year.

The Big Picture: A Market in Transition

The headline for Ontario in 2026 is balance.

For the first time in years, we are seeing a convergence of increased supply and softening demand. On the supply side, government incentives have successfully spurred purpose-built rental construction, with rental starts actually outpacing other housing types.

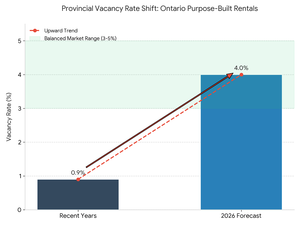

Simultaneously, demand is moderating. Changes to federal immigration targets have led to fewer international students and foreign workers—historically a key demographic for rental uptake. Consequently, vacancy rates across the province are trending upward, expected to settle between 3% and 5% this year. This most notably for SWO as well as the Golden Horseshoe according to CMHC forecasts.

Ontario Markets City-by-City

Real estate is hyper-local, and the "Ontario average" hides a fractured landscape. While the province-wide trend is toward softening asking rents and rising vacancies, the specific risks and opportunities vary wildly depending on your region's exposure to international students, the manufacturing sector, and condo oversupply.

1. Greater Toronto Area (GTA): The Core vs. The 905

The GTA remains the heavyweight, but it is currently a tenant’s market for the first time in years.

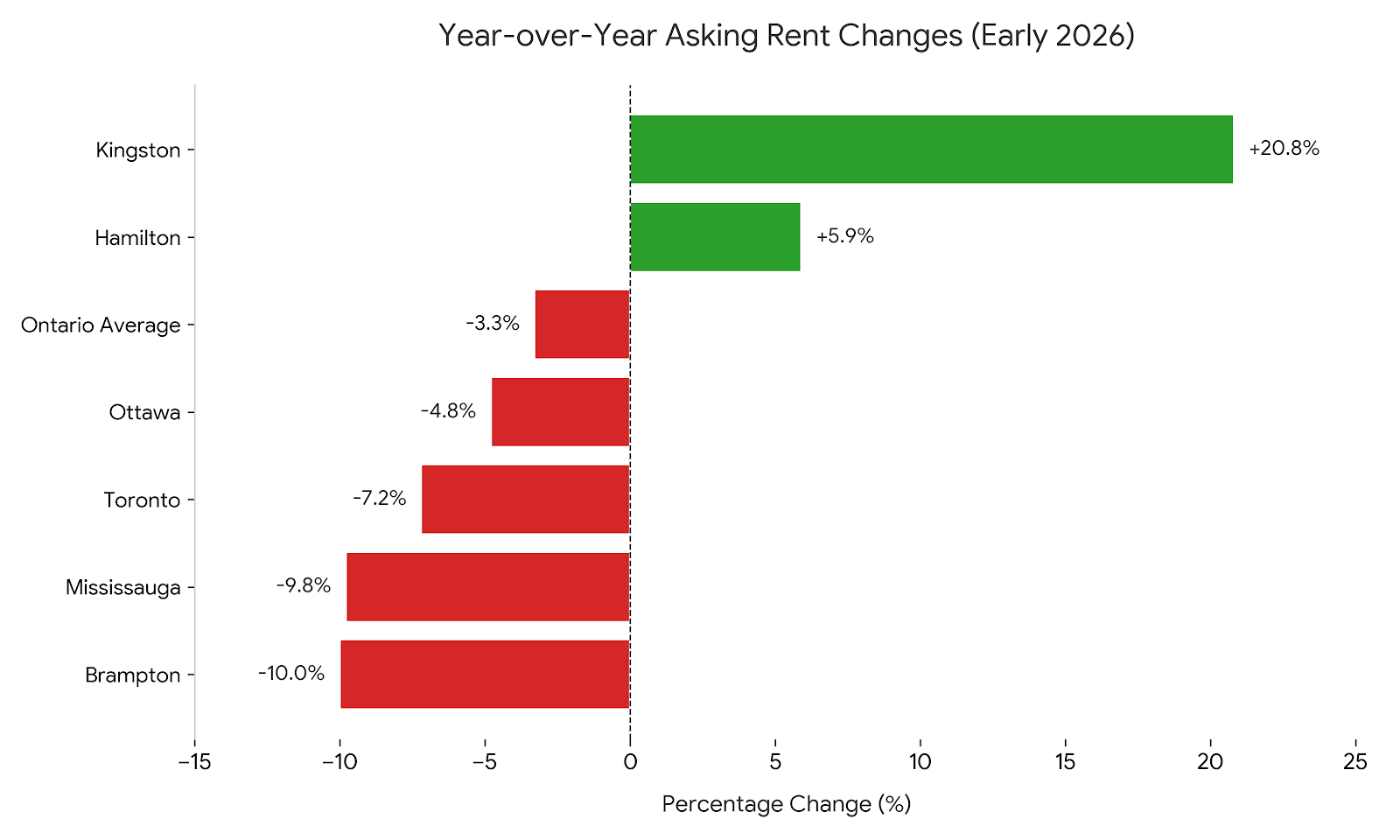

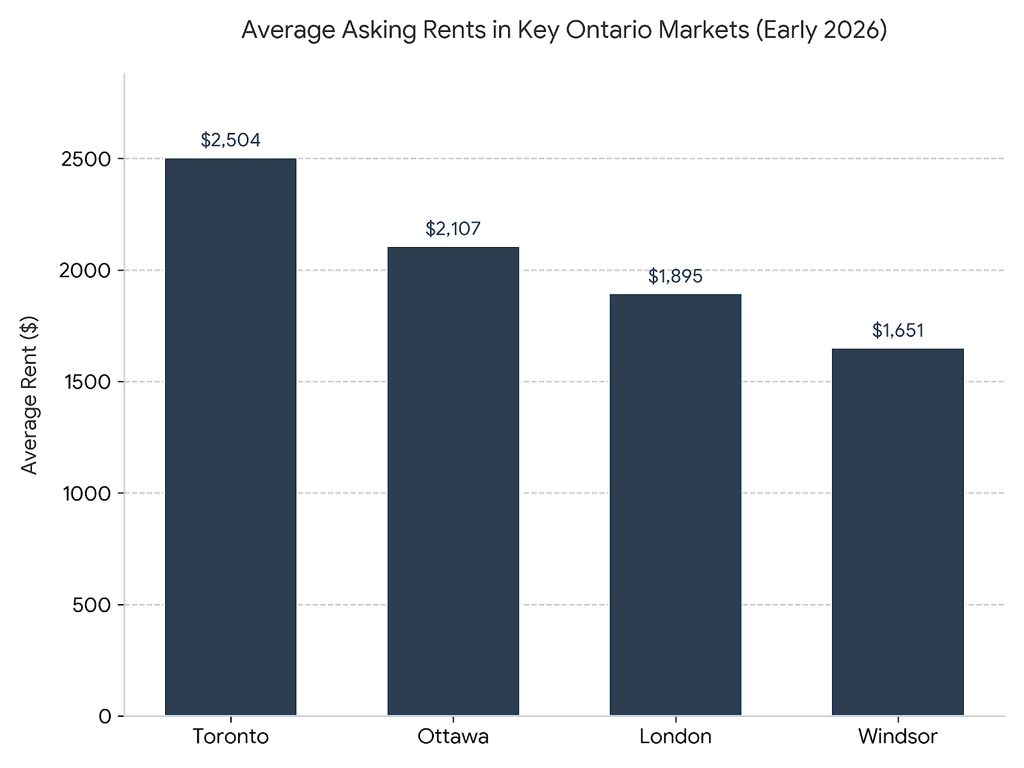

- Rental Rates: Asking rents in the City of Toronto have dropped 7.2% year-over-year to an average of $2,504. The decline is even sharper in the suburbs: Brampton (-10.0%) and Mississauga (-9.8%) have seen double-digit corrections in asking rents as affordability limits were hit.

- Vacancy Trends: There is a distinct divergence in vacancy. The purpose-built rental vacancy rate has climbed to roughly 3%, driven by new supply and students doubling up or leaving. Conversely, the condo rental vacancy rate remains tight at roughly 1%, though this sector faces its own risks with negative cash flow for many investors.

- Landlord Watch: Watch "turnover rents." For the first time recently, rents for turnover units have decreased (down ~2.5%), meaning you may not be able to mark-to-market as aggressively when a tenant leaves.

2. Ottawa: Correcting Faster Than Expected

The capital is easing faster than expected. With a vacancy forecast rising toward the 3.6%–3.8% range, Ottawa is seeing the impact of slowing population growth and a significant number of new units coming online.

- Rental Rates: Apartment rents in Ottawa have fallen 4.8% year-over-year to $2,107. Interestingly, shared accommodation rents in Ottawa bucked the trend, rising 7.4%, driven by new co-living projects entering the market.

- Vacancy Trends: Vacancy is rising faster than anticipated. The cap on international students and foreign workers has reduced demand significantly.

- Landlord Watch: With federal public service cuts looming as a potential risk, employment stability—usually Ottawa's strength—is now a question mark. Expect very modest rent growth, if any, capped by the provincial guideline of 2.1%.

3. Hamilton: The Ontario Growth Outlier

While Toronto and Ottawa soften, Hamilton has emerged as a surprisingly resilient pocket for rent growth, though it is not immune to vacancy creeping up.

- Rental Rates: Hamilton was Ontario’s rent growth leader early this year, posting a 5.9% increase in asking rents. This suggests that as tenants are priced out of the GTA, they are still driving demand in the Hammer.

- Vacancy Trends: Despite strong rent growth, vacancy rates are expected to keep climbing in 2026 as new rental supply and condo completions hit the market simultaneously.

- Landlord Watch: The window to push rents here may be closing as the market balances out by 2027.

4. Kitchener-Waterloo & London: The "Student Belt" Correction

These markets were the hottest in the province just two years ago, but they are most exposed to changes in federal immigration policy.

- Rental Rates: Rents in London are essentially flat, hovering around $1,895. Kitchener-Waterloo-Cambridge is seeing a similar trend, with average prices expected to remain flat throughout 2026 before recovering in 2027.

- Vacancy Trends: Vacancies are rising in both regions. The reduction in international study permits is hitting these university-heavy towns directly, reducing the number of renter households formed.

- Landlord Watch: In Kitchener-Waterloo and the north of Cambridge, infrastructure constraints have paused some new development approvals. Click here for more details. This supply constraint might protect existing landlords from competition in the medium term, even if demand is soft right now.

5. Windsor & St. Catharines: Economic Headwinds

These regions are facing challenges tied to the broader economy and cross-border trade.

- Rental Rates: Windsor is seeing modest rent growth but sits at the lower end of the pricing spectrum at $1,651. St. Catharines-Niagara is seeing improved affordability help sales, but rental demand is tempered by fewer intra-provincial migrants.

- Vacancy Trends: Vacancies are rising in Windsor as the number of work-permit holders—a key demographic for the city—declines.

- Landlord Watch: Windsor is heavily exposed to trade uncertainty. With ongoing tariff uncertainty and the CUSMA review in 2026, manufacturing employment could wobble, which would directly impact tenant solvency.

6. Kingston: The Anomaly

Rental Rates: If you are looking for an outlier, look at Kingston. It ranked first in Canada for annual rent growth, exploding by 20.8%. This is partly driven by an infusion of new, higher-priced supply skewing the averages, but it highlights a market with deep supply constraints.

2026 Forecast: The Numbers

- Vacancy Rates: Expect a province-wide increase. The days of sub-1% vacancy are largely behind us for the near term. Consensus among researchers project broadly balanced conditions (3%+) across most major Ontario CMAs

- Rental Rates: We are witnessing a decoupling of asking rents versus current rents. Asking rents in Ontario dropped 3.3% year-over-year in January 2026. However, average rents (including occupied units) will see modest growth, capped by the provincial guideline of 2.1% for 2026 and turnover adjustments.

- Construction: While overall housing starts are declining due to high costs, purpose-built rental construction remains the primary driver of new supply in Ontario, outpacing condo and homeowner starts

Things Landlords Must Watch in 2026

- The "Turnover" Gap and Tenant Retention With asking rents softening and vacancy options increasing, tenants are becoming more mobile. The gap between market rent and occupied rent is narrowing in some segments, which may encourage tenants to move for better amenities or incentives. Landlords should focus heavily on retention; the cost of turning over a unit in a 4% vacancy market is significantly higher than in a 1% market.

- Delinquencies and Arrears Economic uncertainty remains a headwind. While mortgage arrears are low, we are seeing rising non-mortgage arrears (e.g., credit cards, car loans) in regions like Southwestern Ontario. This is typically a leading indicator of financial stress. Vetting tenant creditworthiness is more critical now than it was two years ago.

- Trade Policy Impacts Ontario’s economy is sensitive to cross-border trade. With the CUSMA review scheduled for 2026 and tariff uncertainty with the U.S., regions heavily reliant on manufacturing (Windsor, parts of the GTA) could see fluctuations in employment, directly impacting rental demand.

The Bottom Line

The rental market in 2026 offers stability rather than aggressive appreciation. For those of us buying and selling multi-residential buildings, this means underwriting must be disciplined. We can no longer bank on double-digit rent growth to solve operational inefficiencies.

If you are looking to review your portfolio or discuss how these trends affect the valuation of your specific building, reach out to me directly.

Check out this article next